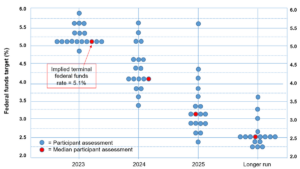

The 25 basis-point increase was accompanied by changes in the Federal Open Market Committee’s statement that imply a possible pause at the Fed’s next meeting in June with a bias toward more tightening should inflation prove sticky.

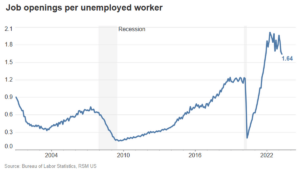

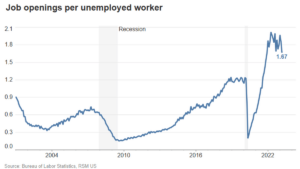

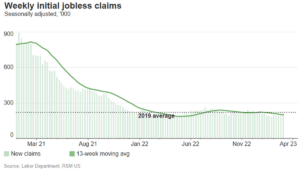

Job openings fell to 9.6 million in March from almost 10 million in February, a clear sign that the labor market is softening as the economy slows down.

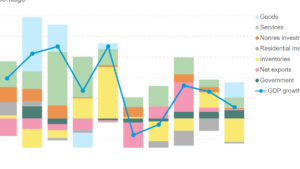

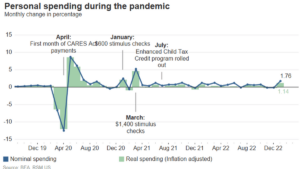

Growth in the first quarter expanded at a 1.1% annualized pace and by 1.6% on a year-ago basis as a modest inventory correction and a large pullback in business investment—a net drag of 2.34%—offset the robust 3.7% increase in overall household consumption.

Job openings and factory orders came in lower than expected on Tuesday, continuing to show signs of softening economic demand that should work in the Federal Reserve’s favor in fighting inflation.

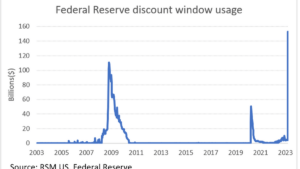

Prices in the money market now suggest increased levels of risk being priced into short-term lending and the tightening of overall financial conditions that was missing until the collapse of Silicon Valley Bank and Credit Suisse.

In the past week alone, the Federal Reserve's loans outstanding to the financial system have ballooned to about $318 billion, up from $15 billion a week ago.

The Fed’s key gauge of inflation—the personal consumption expenditures deflator—rose by 0.6% on the month for both the top-line and the core numbers, bringing the year-over-year inflation to 5.4% and 4.7% for the two series, respectively.

Policy brinksmanship over lifting the debt ceiling and the threat of default it brings is increasing the cost of doing business and carries far more risk than is commonly acknowledged.