Resources

US July CPI: Inflation posts likely peak as commodity, gas and transportation prices fall

REAL ECONOMY BLOG | August 10, 2022

Authored by RSM US LLP

Commodity, oil, and gasoline prices declined noticeably in July, driving the pace of top-line inflation lower even as core inflation continued to increase at a torrid pace. This will provide a large boost to overall consumption and economic activity as Americans likely spent roughly $400 million less on gas compared to the previous month which will result in improved consumption and direct relief to beleaguered households.

While the boost to overall economic prospects is welcome, easing inflation will ring hollow with many down-market consumers whose wages are falling in real terms despite the decline in gasoline prices alone adding about $400 million dollars back to household balance sheets.

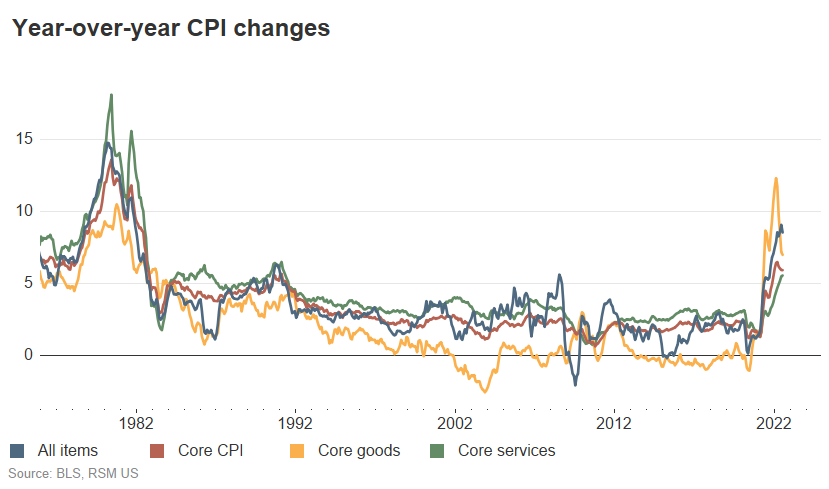

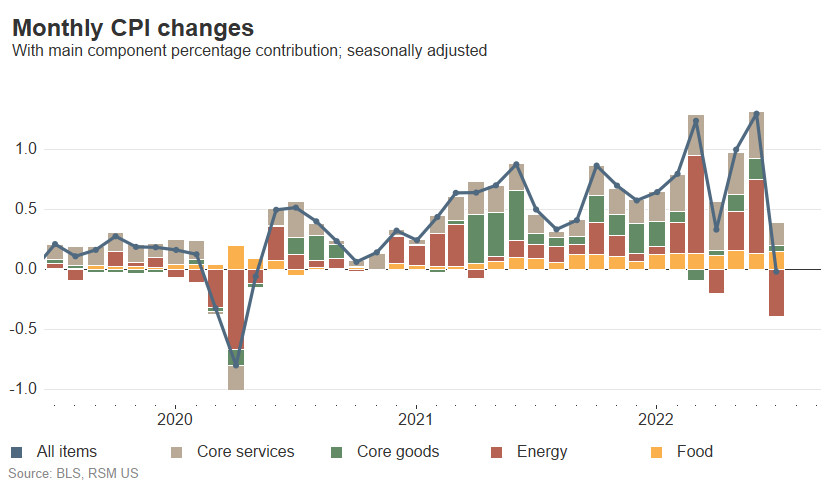

Topline inflation as measured by the consumer price index was flat; it did not increase or decline on a month-over-month basis, which translated to an 8.5% increase on a year-ago basis, Labor Department data released on Wednesday shows. Core prices, excluding the volatile food and energy components, advanced at a 0.3% pace in July and 5.9% increase over the past year. Interestingly, transportation costs declined 2.1% on the month, airfares fell 7.8% and commodities, excluding food and beverages, dropped 1.4%. Many of the pandemic-induced increases in overall pricing are, for now, declining.

Falling input prices and the 19.3% drop in gasoline prices since the June 16 peak, which declined 7.7% in the July consumer price index, should bolster overall economic activity and household and corporate sentiment in the current quarter, even though the current inflation shock has yet to be absorbed by the economy.

While the boost to overall economic prospects is welcome, easing inflation will ring hollow with many down-market consumers whose wages are falling in real terms despite the decline in gasoline prices alone adding about $400 million dollars back to household balance sheets.

The economic inequality that has colored the domestic economy for roughly fifty years is clearly resulting in a bifurcation in the reaction function of American households and their ability to absorb and adjust to that inflation shock. The upper two quintiles of income earners—those earning above roughly $110,000 and then $250,000 per year and responsible for approximately 62% of spending—appear to be brushing aside the sharp increase in prices without too much of an adjustment. The pain quotient in the three lower quintiles can clearly be observed via the demand destruction in consumption of gasoline that is in part a portion of the economic narrative around growth prospects for the economy in the second half of the year.

This data will not alter the path of monetary policy out of the Federal Reserve, which in our estimation needs to lift the policy rate to at least 4% before it considers pausing to ascertain the adjustment of the economy to the shift in policy to obtain price stability. We expect a 75-basis-point hike at the September meeting due to the hot labor market and the broadening of inflation into the housing sector, which is now a large part of the policy challenge. Given the long and variable lags associated with changes in monetary policy (the previous two 75-basis-point hikes have not worked their way through the real economy), ideas of a near-term pause or even a reversal in policy due to the demand destruction are not aligned with the reality of the inflation data, despite the probability that June 2022 may represent the peak in the current pricing cycle.

The data

Overall energy costs dropped 4.6% in July, while energy commodities declined 7.6%, which underscores the large drop in oil and gasoline costs observed since June. Services costs advanced 0.3% on the month are up 6.2% compared to one year ago.

In contrast with the price declines in the energy complex, housing, which comprises 41.72% of the overall index, advanced 0.4% in July, which is below the three-month average of 0.6%, and up 7.4% on a year-ago basis. Shelter costs advanced 0.5% and the policy sensitive owners equivalent rent of residences increased 0.6% in July. Shelter costs are up 5.7% and OER residences are up 5.8% compared to one year ago.

From our perspective the costs inside the housing complex have not yet finished increasing and it will likely be some months before an apex is reached.

Food costs continued their steady march higher, increasing by 1.1% in July. They are now up 10.5% from one year ago. Apparel costs declined 0.1% on the month, the cost of new vehicles increased 0.6%, and used cars and trucks declined by 7.8%. Recreation costs increased 0.3%, education costs dropped 0.2%, and overall commodity costs fell by 0.5%.

The takeaway

While it is fair to state that we may have observed the apex in overall inflation in June 2022, the risk to the economic outlook remains inflation, and the direction of policy needs to remain in place. The July data implies that past Federal Reserve policy is making an impact; the objective of a return to price stability requires the Fed stick with its policy path.

While we are encouraged by the easing in commodity, energy and gasoline prices, the 10.5% increase in food and the 7.4% jump in the cost of housing both will continue to act as a drag on overall household disposable income. In our estimation, it will be two to three years before inflation is anywhere near the Fed’s 2% inflation target.

Let's Talk!

Call us at (325) 677-6251 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-08-10.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/us-july-cpi-inflation-posts-likely-peak-as-commodity-gas-and-transportation-prices-fall/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Condley and Company, LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Condley and Company can assist you, please call (325) 677-6251.