Resources

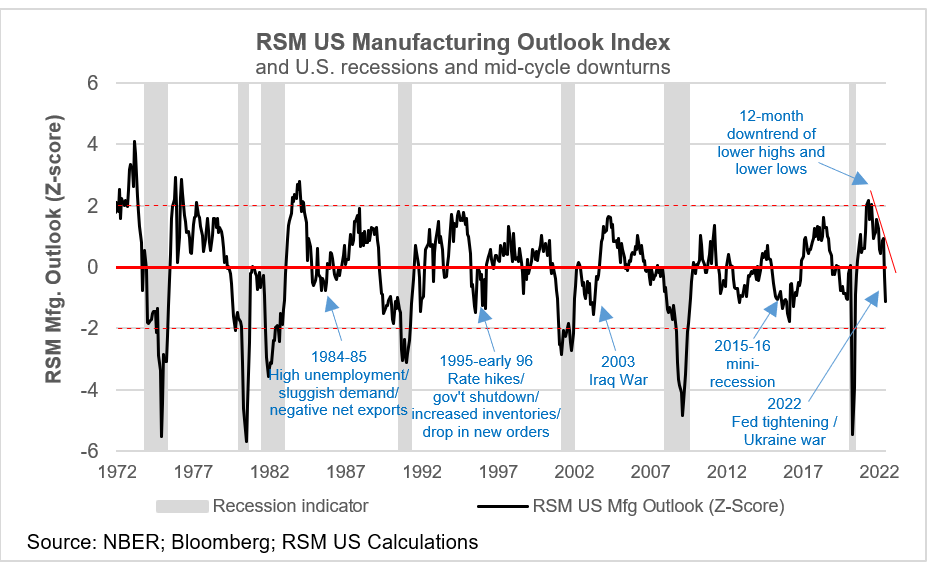

RSM US Manufacturing Outlook Index shows a slowing industrial sector

REAL ECONOMY BLOG | June 29, 2022

Authored by RSM US LLP

The RSM US Manufacturing Outlook Index declined in June, signaling a slowdown in overall economic activity. The reading of 1.1 standard deviations below normal suggests that tighter financial conditions and the energy shock are taking a toll on the industrial sector.

Our index is a composite of surveys of current manufacturing activity conducted by five regional Federal Reserve banks. Three of the regional surveys are now reporting outright contractions and the other two are falling quickly toward contraction.

Three surveys by regional Federal Reserve banks are now reporting outright contractions.

Whether this downturn spreads to the rest of the economy will depend on external events and the impact of action by the monetary authorities to squash inflation. We think there is a 45% probability of a recession over the next 12 months.

But even with the reported downturn in current production and diminished expectations for activity this year, employment in manufacturing continues to expand, as do intentions for capital investment.

That suggests the potential of a less harsh outcome for the manufacturing sector if monetary authorities continue to clamp down on inflation and if a recession were to come to pass, as was the case in the 2020 pandemic recession.

Still, the manufacturing sector remains vulnerable to drastic changes in monetary policy and events like the recurring oil crises or the pandemic closings in China that can send a shock wave through the economy.

The business cycle has never been smooth or consistently short or long, and we can’t expect this one to be any different.

Regional results

Manufacturing activity in New York State held steady, according to a survey conducted from June 2 to 9. In fact, 28% of firms reported that conditions had improved over the month, and 29% reported that conditions had worsened.

New orders and shipments indices climbed back into positive readings, but the unfilled orders index fell to its first negative reading in over a year while inventories expanded.

Manufacturers reported a solid increase in employment, and prices paid increased. Optimism about future conditions was subdued for a third consecutive month, but capital spending and technology spending plans remained firm.

All this points to the difficult challenges facing the Federal Reserve—achieving price stability while keeping people in their jobs.

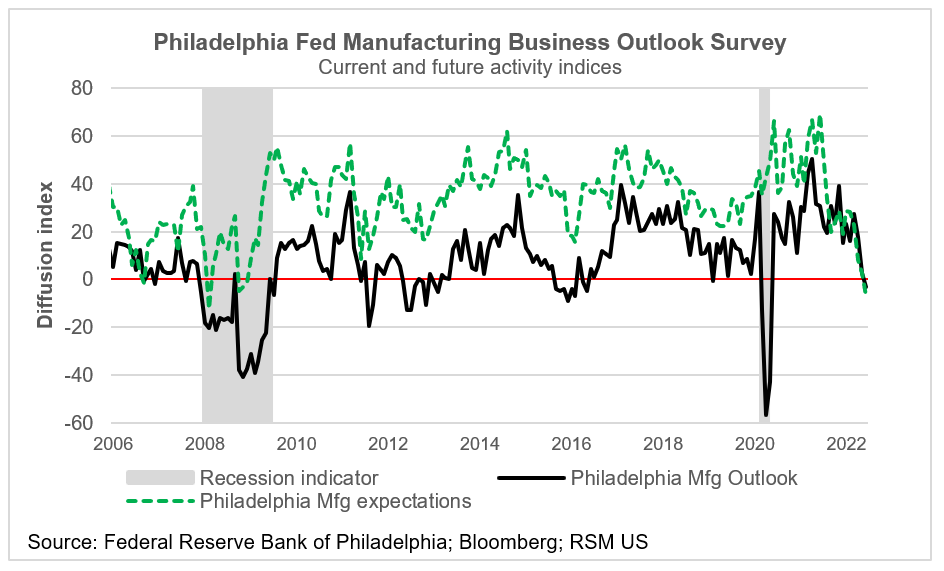

Current manufacturing activity in the Philadelphia region deteriorated for the third month in a row and was negative for the first time since May 2020. Manufacturers’ expectations for the next six months declined for the fifth consecutive month.

In the survey conducted from June 6 to 13, indicators for new orders and shipments decreased sharply and prices remained elevated. Still, firms continued to report increases in employment, with only 3% reporting decreases.

Responses to special questions found that 72% of firms experienced increased production relative to the first quarter, and nearly all firms reported constraints on capacity utilization stemming from worker shortages and supply chain problems.

Manufacturing activity in the Kansas City Fed’s Tenth District slowed further but remained positive, while expectations for future activity moderated slightly.

The survey found that more than 85% of firms reported delays in shipping and product availability as having a negative impact on their business activity, with around half of firms not expecting any improvements in the next six months.

The report pointed to decreased activity at durable goods plants in June, especially electrical equipment, transportation equipment and furniture-related product manufacturing. Indices for production, shipments, new orders and order backlogs declined, while inventory indices increased slightly.

In response to special questions, about 60% of firms expected supply chain disruptions and shortages to remain unchanged or worsen in the next six months.

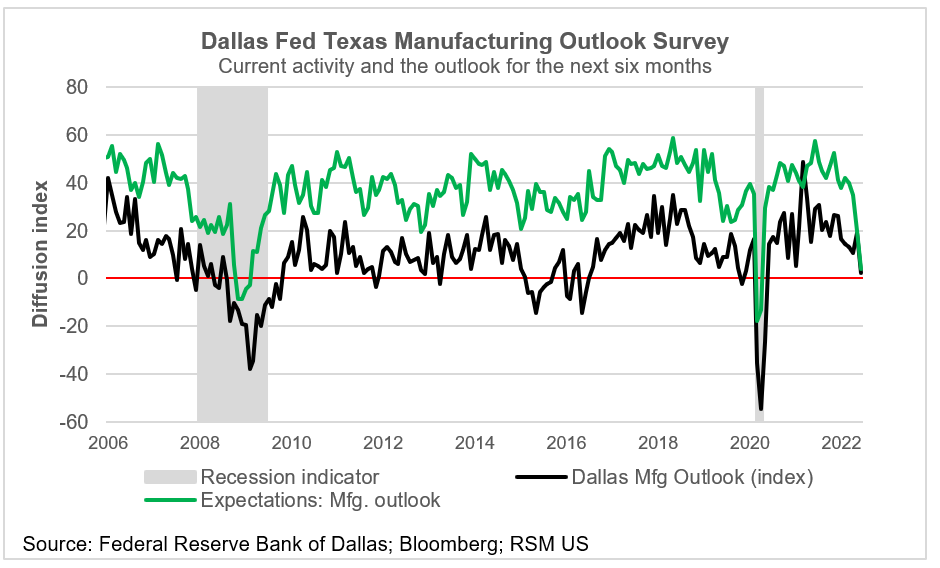

Growth in Texas factory activity decelerated sharply in June, reaching its lowest reading since May 2020, according to the Texas Manufacturing Outlook Survey conducted from June 14 to 22. In addition, respondents were notably less optimistic regarding future manufacturing than in May, with both the current and future production indices now barely positive.

The new orders index turned negative for the first time in two years, signaling a decline in demand. Indices for capacity utilization and shipments remained positive but fell markedly.

Firms continued to report above-average employment growth and longer workweeks. Nearly a quarter of firms, or 24%, reported net hiring against only 9% with net layoffs. Wages continued to increase strongly as did input prices.

In special questions, firms expected wage growth of 7.4% this year, followed by 6% growth next year. Just over half of firms, or 51%, considered supply chain issues to be restraining production, and 41% of firms cited staffing shortages as limiting operating capacity.

Manufacturing firms in the Richmond Fed’s Fifth District reported a sharp decline in activity in June. Firms reported severe drops in shipments and orders and in local business conditions, while noting an increase in employment both in the current month and over the next six months. The report was released on June 28.

Supply chain issues appeared to be in decline as well, as firms reported improvements in inventories and vendor lead times.

Let's Talk!

Call us at (325) 677-6251 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-06-29.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/rsm-us-manufacturing-outlook-index-shows-a-slowing-industrial-sector/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Condley and Company, LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Condley and Company can assist you, please call (325) 677-6251.