Resources

Preparing for a tsunami of imported goods

REAL ECONOMY BLOG | June 28, 2022

Authored by RSM US LLP

The recent reopening of China’s factory floors and the easing of its supply chain bottlenecks have prompted discussion about the ability of the U.S. supply chain to absorb what will be a tsunami of imported goods.

With the value of the dollar rising, which lowers the cost of imported goods, demand for foreign-produced goods will increase.

But there are other factors at play, including seaport capacity, shipping costs and transportation sector employment–that will shape how the import picture shakes out in the months to come.

Despite the deficiencies of the domestic supply chain, we think that there is a reduced risk of another round of supply chain-induced price increases and inflation because of changes made at the ports and by private sector firms over the past two years.

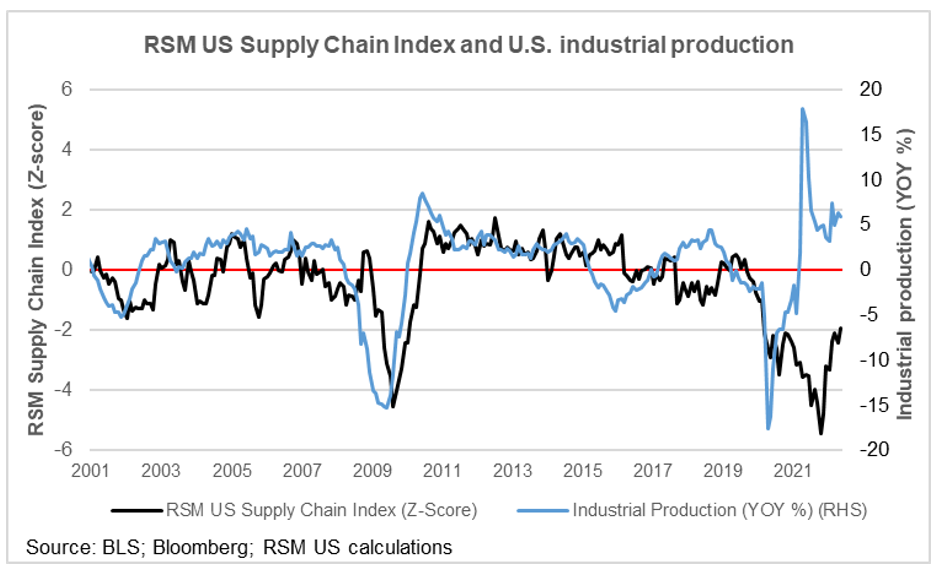

As of May, the RSM US Supply Chain Index remains significantly below normal levels of operation, and that should be considered a grave problem. Yet U.S. industrial production began its rebound more than a year ago and has grown at an average yearly rate of 5% over the past 12 months.

Circumstances have changed. Manufacturers have looked to alternative providers for intermediate goods and, with fuel oil prices so high, have shortened their supply lines.

The increase in industrial production also implies that consumer choices are changing as well, with local suppliers making more and more sense.

Because the decades-long neglect of the U.S. transportation system has not been reversed, the renewed flow of goods into U.S. seaports and air terminals will create a slowdown in economic activity. That slowdown will more likely be the result of monetary policy tightening and geopolitical tensions.

In addition, we should consider the surge in imports as a welcome sign of activity in the global and U.S. economies. In recent decades, it was increased domestic spending that kickstarted the global economy and provided our trading partners with the cash to buy U.S. products and assets.

In this cycle, our trading partners that purchase our financial products, value-added goods and technologies are likely to be a critical difference between a midcycle slowdown and a recession over the next 12 to 18 months.

Seaport capacity

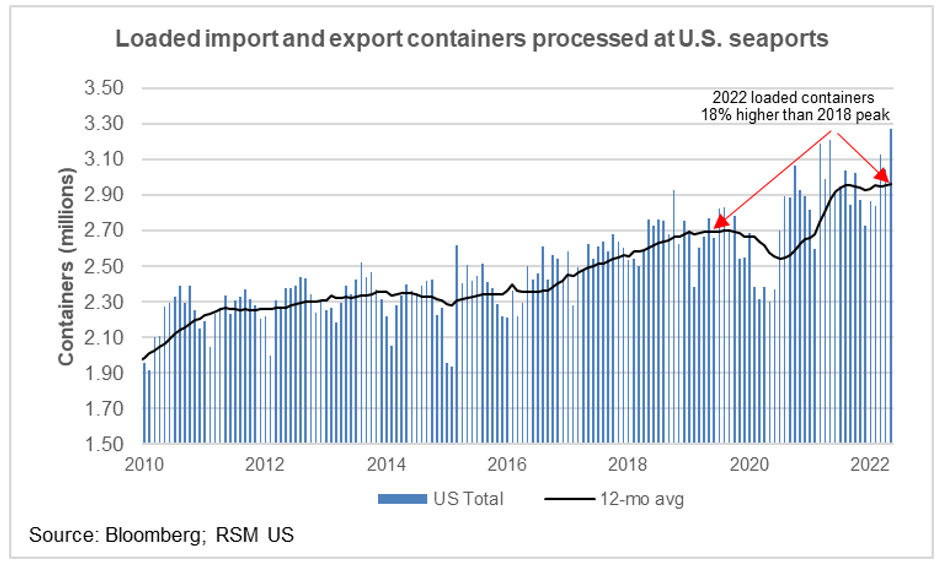

U.S. seaports are now processing 18% more import and export shipping containers than in the months before the 2018 onset of the trade war. All else being equal, this implies that seaports have increased their capacity at an average annual rate of 4.3%.

Whether through efficiencies or expansion, this increased capacity should be sufficient to handle the normal demands of a growing economy. And it would be difficult to expect any private business to expand such that it would be able to meet a once-in-a-lifetime surge in activity.

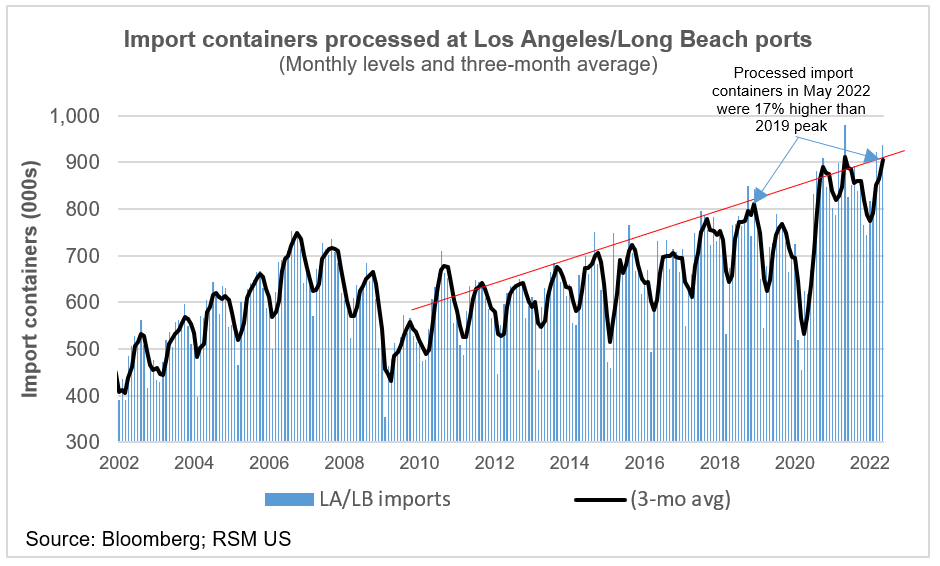

The seaports of Los Angeles and Long Beach have recently shown an increased ability to handle imports from Asia, processing nearly 900,000 import containers per month, which is about 17% higher than their 2019 pre-pandemic peak.

This recent rise put the Southern California seaports back in line with the overall rebound from the 2008-09 economic downturn.

All in all, the question of whether the reopening of China will cripple the domestic supply chain and lead to further increases in the consumer price index cannot be answered by increased capacity at seaports alone.

Shipping costs

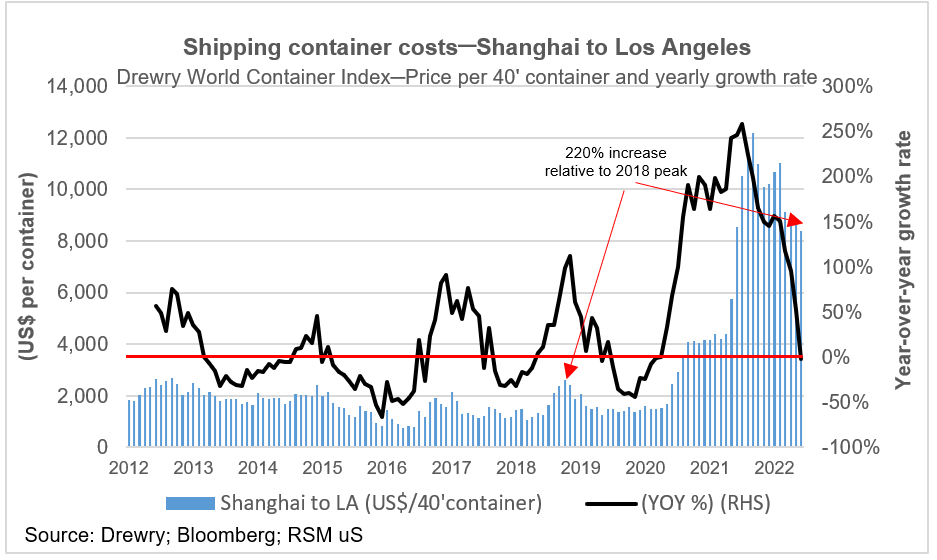

At its peak in late 2018, it cost $2,600 to ship a 40-foot container from Shanghai to Los Angeles. That same container now costs $8,700—3.2 times higher.

Consider also that crude oil prices have increased by 70% over that same period, which raises the cost of moving intermediate and finished goods and prompts producers and wholesalers to shorten their supply chains.

Still, shipping costs have been retreating, particularly since February. This decline is perhaps in response to the decreased ability of Shanghai to handle containers during the latest wave of infections and increased competition among idled ships.

As for predicting the cost of shipping in the coming months, on the one hand there will likely be idled ships competing for work and there is also the possibility that the price of oil will drop if central banks slow demand for goods and services.

On the other hand, the price of crude is likely to remain high for as long as the war in Ukraine goes on.

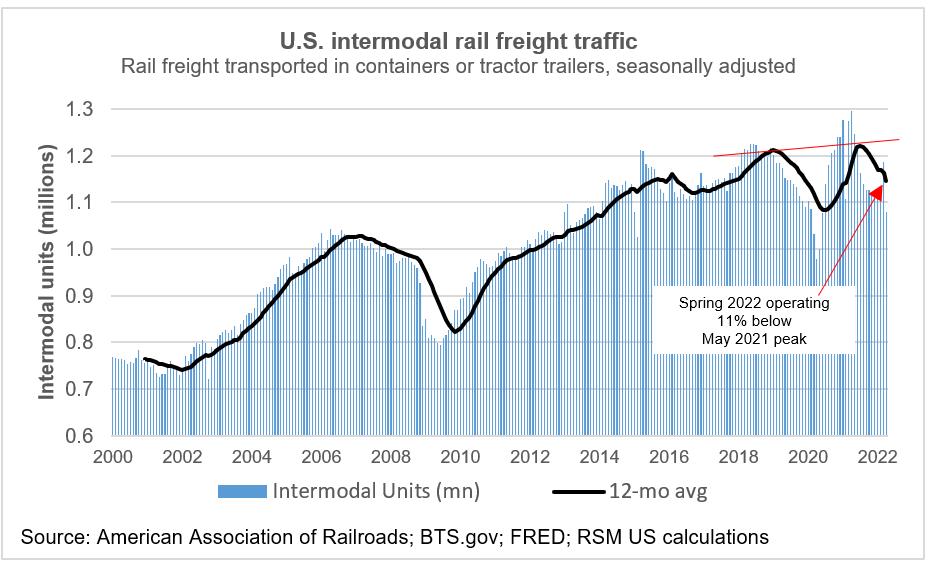

Getting the containers to market

Intermodal freight traffic is operating upward of 11% below peak capacity reached in May 2021, according to American Association of Railroads data through April. That implies slack in the system that could absorb at least some of the expected surge in deliveries to West Coast seaports.

In the longer run, the Department of Transportation has funding to modernize our freight infrastructure, but we can only expect that to help at the margin in the short run.

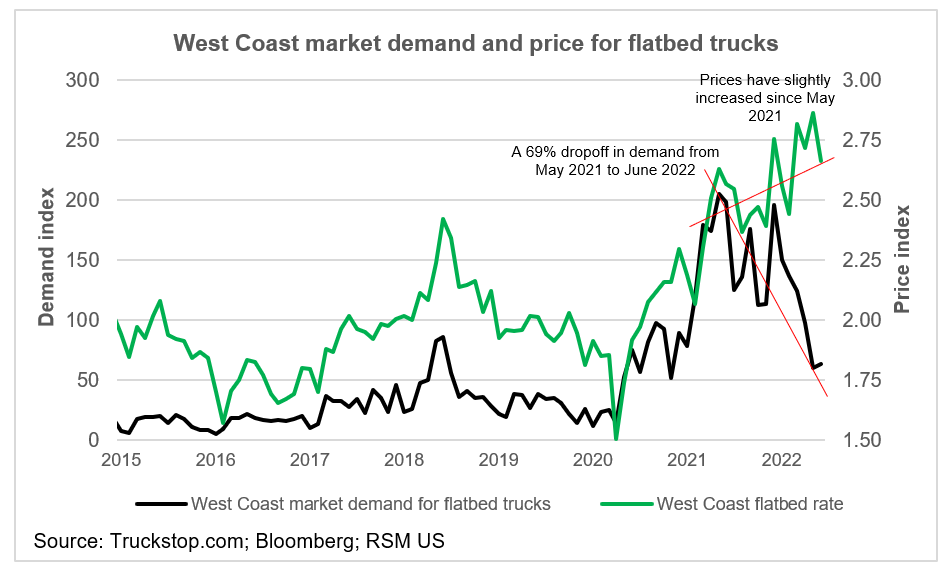

The demand for flatbed trucks along the West Coast has dropped by 69% since peaking in the spring of 2021 as the economy first reopened. Prices, though, have increased, which we attribute to the increase in the price of diesel.

Translating that drop in demand into a greater availability of trucks is probably not that straightforward. That will most likely depend on profitability of truckers and the willingness of new drivers to enter the field.

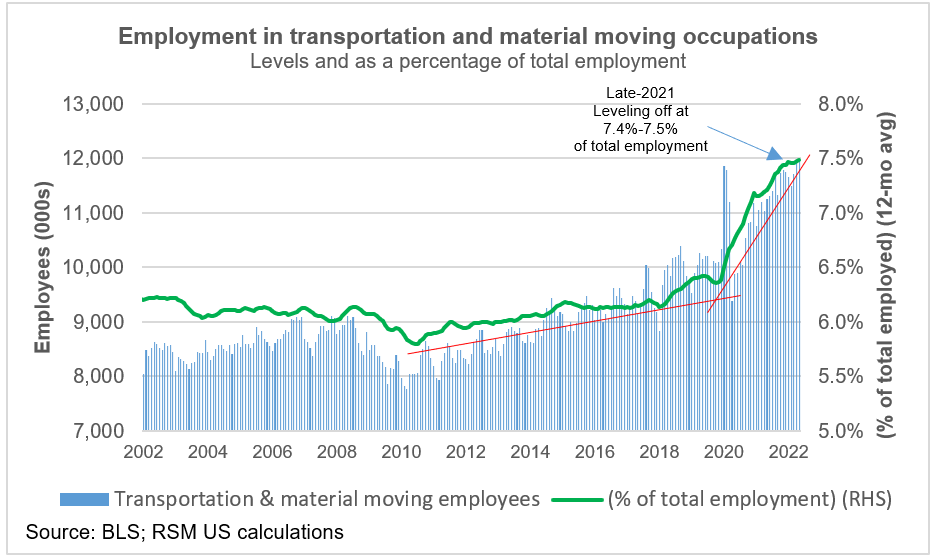

The ability to move goods from the seaports to the warehouses to shops depends on the supply of labor. At the moment, 7.5% of U.S. occupations—or one in 14 Americans—are employed in moving something from one place to another.

That’s up from the recent low point of 5.5% during the Great Recession and is substantially higher than two years ago, earlier in the pandemic.

Since March 2020, when the pandemic shutdowns first hit, there has been an increase of 750,000 people employed in the transportation industries. But there is no guarantee that those trends will last.

There are signs of transportation jobs leveling off in recent months, which might have more to do with China’s pandemic shutdowns than with U.S. employment opportunities. Still, maintaining the labor supply and the attractiveness of the logistics industries will depend on the availability of higher wages in other occupations.

Rebuilding inventories

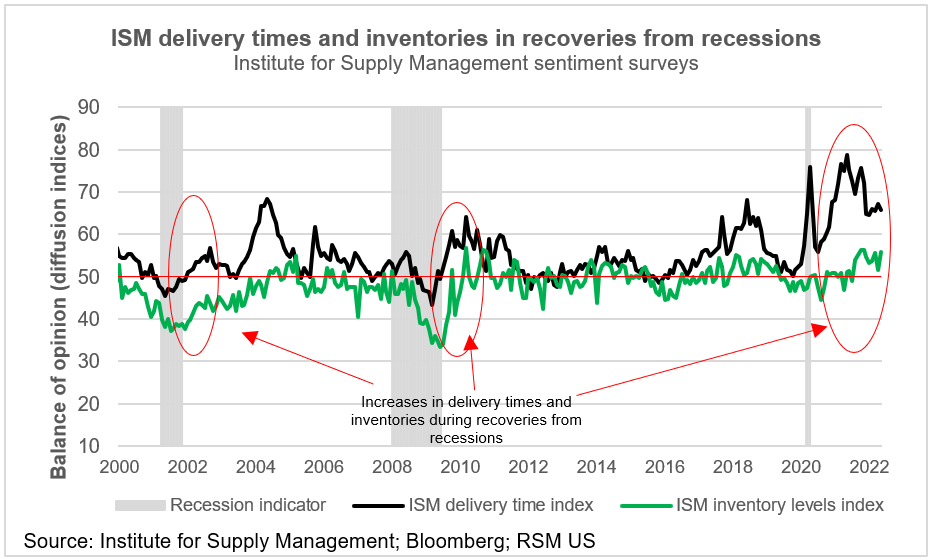

Delivery times are increasing once again, according to surveys by the Institute for Supply Management, which is concerning after improvements of previous months and shows that logistics remains a bigger problem. On the bright side, the ISM surveys suggest that inventories are being replenished, which should provide a buffer for increases in demand.

Let's Talk!

Call us at (325) 677-6251 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-06-28.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/preparing-for-a-tsunami-of-imported-goods/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Condley and Company, LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Condley and Company can assist you, please call (325) 677-6251.