Resources

Inflation and gross margins—who is winning? Part 1: The transportation sector

REAL ECONOMY BLOG | June 07, 2022

Authored by RSM US LLP

RSM took a detailed look at gross margins across different peer groups in the industrials sector to see how each has fared during this time of high inflation. In this article—part of a series—we examine margins for the transportation sector. Here is what we found.

The industrials sector played a significant role in driving the consumer price index up 8.3% in April from the same time in 2021. The largest increases within the sector have come from transportation, motor fuel and energy.

While it's clear that high inflation is leaving its mark on industrial companies, less clear are the different ways subsectors within this space are faring—for better or for worse. We analyzed gross margin data to see whose margins were maintained, grew or shrunk, and where we see them going in the future.

We also analyzed which peer groups are controlling costs, absorbing them or passing them on to customers.

In our analysis of data from Bloomberg, we use Dec. 31, 2019, as a starting point before the pandemic, and reviewed periods up to the most recent available quarterly data, which for most companies meant data through March 31. We selected enough companies from each sector to provide a meaningful representative share of market.

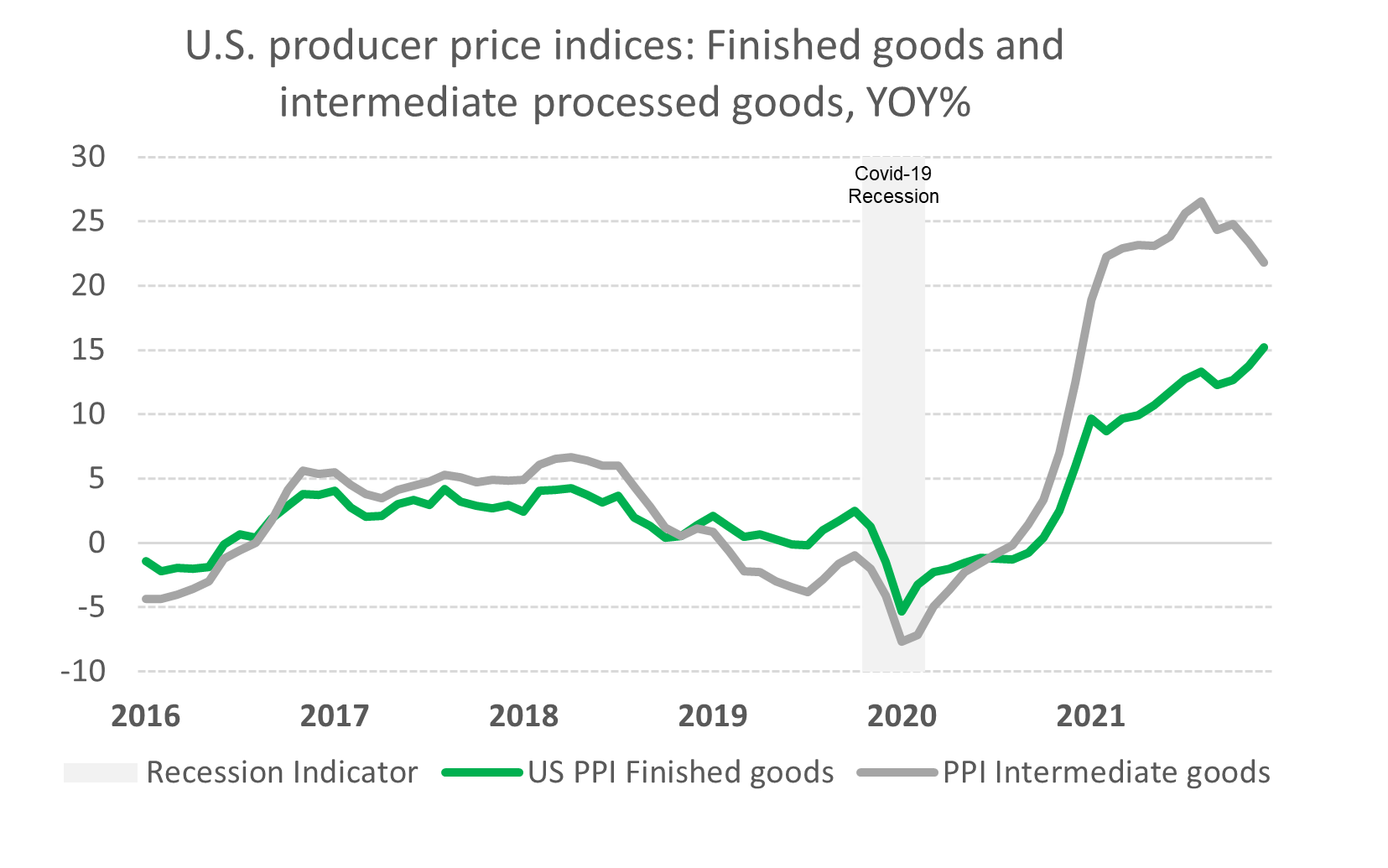

Producer price indices

As a starting point, it is useful to examine producer price indices to understand increases and decreases in prices companies paid to producers for finished goods and intermediate goods.

Producer price indices on intermediate goods eased somewhat from November 2021 through March 2022, indicating that finished goods prices may soon follow. Both gauges are still at highs not seen since the 1970s and have to decline a fair amount before normalizing.

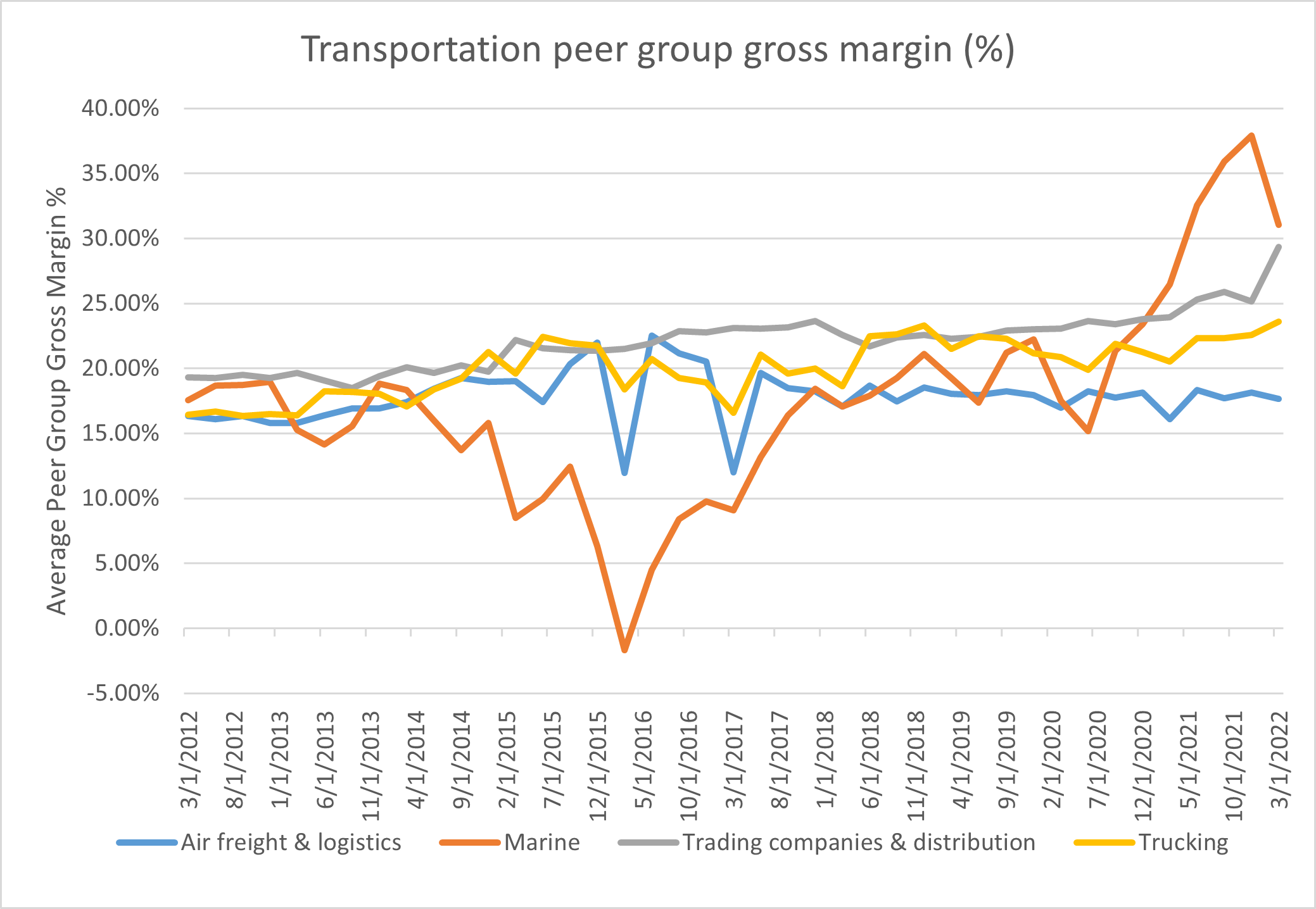

Transportation

Marine transport had the largest gross margin increase of any peer group we examined. Average gross margins for the top 25 marine transport businesses increased from 21.2% just before the pandemic to a peak of 37.9% at the end of 2021, and slid to 31% by March 31.

The price hikes in marine transport recently spurred a bipartisan bill called the Ocean Shipping Reform Act, an effort to limit such hikes in the future. Marine spot rates to transport containers increased as much as five times for some routes in 2021.

We expect average gross margins in this sector will ease in 2022 as shocks work their way through the system. Still, we anticipate marine transport prices will remain elevated relative to pre-pandemic levels throughout 2022 and part of 2023 due to shipping container backlog and high prices for fuel. The easing of recent COVID-19 lockdown restrictions in Shanghai in late May and early June also means the cargo ships that were logjammed at the port there will soon make their way to the United States. The reopening in Shanghai and other parts of China will sustain high container volumes in the already busy summer shipping season.

The continued elevation in marine transport rates will drive more end markets to incorporate surcharges into contracts and hike prices. Due to intricate global supply chains and the time required to transport goods in this channel, price hikes will be sticky for some months beyond when rates do subside.

Average gross margins for air freight and logistics companies increased less than 2% since before the pandemic, ending at 19.2% at the end of March. This sector easily passes higher fuel costs through to customers by linking fuel surcharges to indices that update at regular frequencies.

Similarly, average gross margins for a peer group of 19 trucking companies rose around 3% to 24.1%. Larger trucking firms included in our analysis use fuel surcharges in their contracts and are able to buy diesel at wholesale prices. Prices in both of these sectors will continue to closely follow energy pricing and market demand.

Smaller trucking companies, however, are suffering. These are businesses that have six or fewer trucks on average and buy gas at the pump spot price. Due to their small size they typically don't include fuel surcharges in contracts. These smaller firms are experiencing serious margin pressure as a result—and for some it has created an existential threat to their business.

In the trading and distribution space, average gross margins across 33 businesses rose from 23% at the beginning of the pandemic to 31.2% at the end of March. Trading and distribution companies are having an easier time increasing prices and are more than making up for increases in cost. The economy's shift from services to goods has also given them a boost. The future margin expectations of this sector will depend on continued demand for goods—which has eased due to reopenings in the service sector—and on signs of an economic slowdown as the Fed tightens the money supply.

The takeaway

Overall we expect some of the transportation sector pressure to ease in 2022 but remain elevated into 2023. The biggest risks will come from the European Union shunning Russian oil—causing increased global fuel costs—and impacts from the recent COVID-19 lockdown in Shanghai. Labor, which was an issue for trucking before the pandemic, has been made worse by it and will continue to be a factor. Still, these effects may be somewhat offset by an economic slowdown.

Let's Talk!

Call us at (325) 677-6251 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Matt Dollard and originally appeared on 2022-06-07.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/inflation-and-gross-margins-who-is-winning-part-1-the-transportation-sector/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Condley and Company, LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Condley and Company can assist you, please call (325) 677-6251.