Resources

How lumber tells the story of home building during the pandemic

REAL ECONOMY BLOG | June 15, 2022

Authored by RSM US LLP

RSM took a detailed look at gross margins across different peer groups to see how each has fared during this time of high inflation. In this article—part of a series—we examine margins for timber companies, lumber producers and homebuilders. Here is what we found.

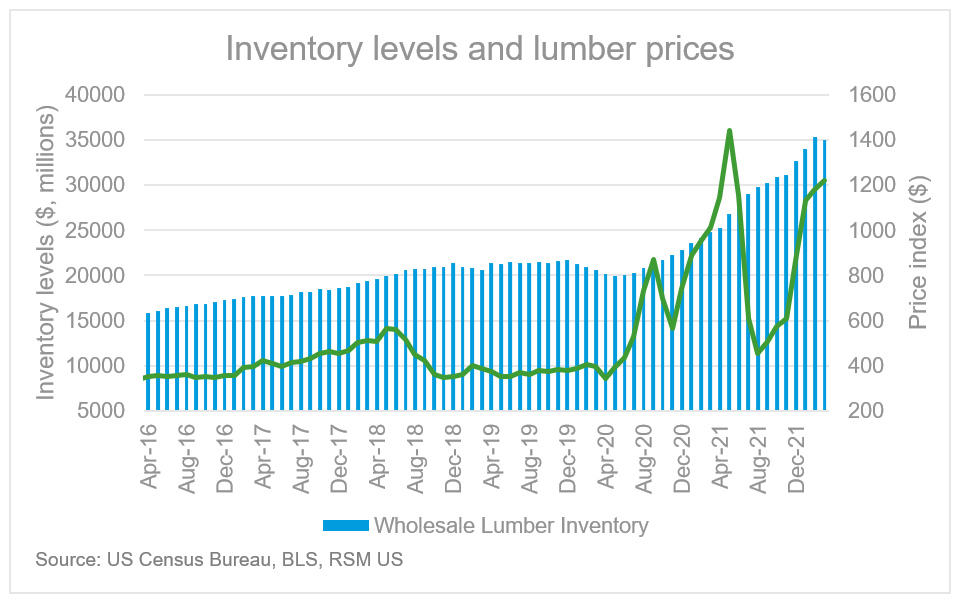

Lumber prices have had a tumultuous two years. Since March 2020, lumber futures rose 359%, declined 68%, rose again 159% and declined 55%. Despite the roller-coaster ride, lumber prices are still significantly higher than they were before the pandemic, with futures in May nearly double where they were before the pandemic.

The increase has been blamed for the rising price of new homes during the pandemic, with the National Association of Home Builders noting in April 2021 that the increase in lumber prices alone was responsible for adding as much as $36,000 to the average price of a new home.

But that prompts a question: With lumber prices declining, why hasn’t the cost of a newly built home declined as well? Part of the answer lies in the scale that large developers have and how this size has allowed them to endure the ebbs and flows of the market. It’s a different story for smaller builders, though, which have been more vulnerable to the swings of input costs like lumber.

To understand this dynamic, consider what happens with a piece of lumber as it goes from the forest to a construction site, and how the biggest builders reap the biggest rewards.

The timber companies

The journey for lumber begins anytime from 25 to 50 years before the tree is harvested. A tree is planted in one of the approximately 200 million acres (about the area of Texas) of commercial forested timberlands in the United States. Most of this land is owned by private individuals or corporations, but there are three primary publicly traded real estate investment trusts that control 10% of the timberland.

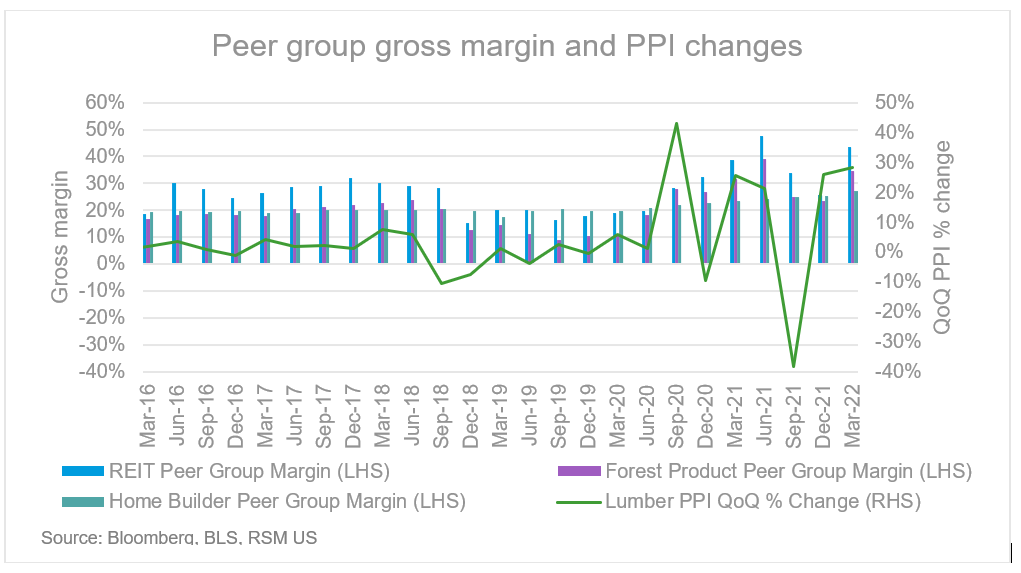

As lumber prices rose throughout the pandemic, margin prices among the investment trusts soared, with average gross margins hitting close to 48% in June 2021, double the pre-pandemic three-year average gross margin of 24%. (For our analysis of gross margins, we selected enough companies to provide a meaningful representative share of market in each sector.)

The increase in margin is reflective of supply challenges that the industry faces. Aside from the United States, one of the other major sources of timber is British Columbia. In the early 2000s, British Columbia was devastated by a pine beetle infestation, and the response was to salvage as much lumber as possible. This drove up supply right before the financial crisis. The combination of muted demand and high supply forced many Canadian loggers out of business, reducing competition.

Now, with demand for lumber soaring, the United States doesn’t have much excess timber capacity, allowing for these large REITs to effectively raise prices unencumbered.

Smaller and midsize timber companies, by contrast, have struggled. Loggers do not have a large marketplace to sell their lumber to different sawmills or timber buyers. Instead, loggers harvest lumber for a specific mill or timber buyer on a contract basis.

Sometimes these buyers will place quotas on the loggers, limiting them to bringing a certain tonnage of lumber to sell at the mill for a designated period. These quota systems serve as a means for limiting excess harvesting and guarantee prices to these sellers.

But the quotas are often not set in stone, changing on a weekly or even daily basis. With the shortage of truck drivers, these loggers are feeling a pinch because they are limited in what they can sell to each sawmill and there are not enough drivers to deliver their logs to sawmills outside of the local areas, which is limiting production.

The producers

Once the timber is harvested, it is sent to the sawmill, where the lumber is cut. Early in the pandemic, sawmills cut back on production because of the health crisis itself and also because producers thought that demand for lumber would plunge, as it did during the financial crisis in 2008.

This prediction proved to be inaccurate, though, as demand surged. At the pandemic’s onset, this left many sawmills underproducing. However, by the fall of 2020, many of the publicly traded forest companies were back up and running, humming with orders, which enabled them to expand their average margins from a pre-pandemic five-year average of 17% up to 48% by the second quarter of 2021 (based on a select peer group of American and Canadian forest product companies).

By the summer of 2021, inventory levels began to improve across the resellers, driving down lumber pricing and margins for forest product companies, with gross margins of the average peer group dropping to 26%. The declines were short lived, though, as speculation began to enter the market, because of the large focus placed on homebuilding throughout the pandemic.

Now, we are again seeing a drop-off in lumber prices. With the Federal Reserve raising interest rates to tame inflation, demand for building products will continue to ease as home builders look to cope with demand cooling to more normalized levels.

These factors should bring lumber prices back in line with long-term price trajectories before the pandemic and serve to tighten up margins back to pre-pandemic levels.

The builders

Housing has been one of the largest inflationary pressures in the economy, rising by 21.5% year over year as of March, according to the S&P CoreLogic Case-Shiller National Price Index.

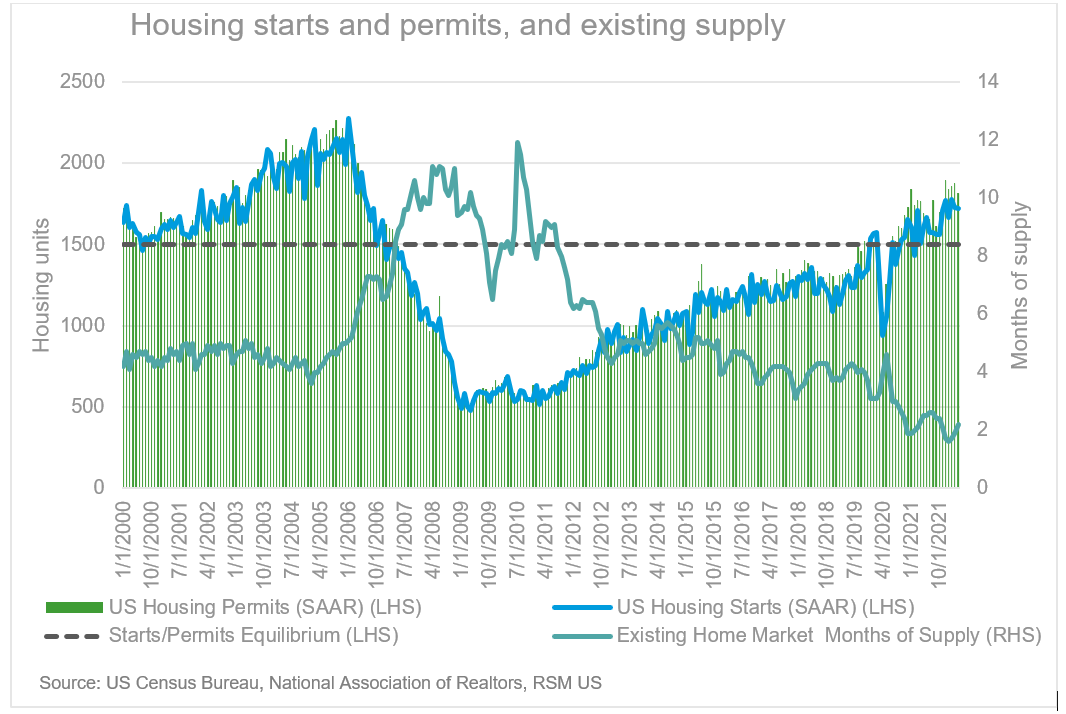

Builders have benefited on both the supply and demand fronts. On the supply front, the United States has underbuilt homes since 2007, because many builders did not want to get caught with excess inventory the way they did after the Great Recession. This underbuilding—the nation is about 5 million homes short of what it needs—coupled with the emergence of millennials as a buying force over the past decade has led to a steep decline in inventory levels.

This shortage was further worsened by significant growth in demand pushed by the Fed’s lowering of interest rates in 2020 to combat the pandemic, along with peoples’ want for more home space to live and work.

Now, with the Federal Reserve raising interest rates, builders will need to approach the next year with caution. The existing-homes market, which is about 10 times larger than the market for new homes, is heavily undersupplied with inventory levels, measured by months of supply, at 2.2 months. The new home market, however, is at 6.4 months. Equilibrium for these markets is typically between four and six months.

Large publicly traded home builders have been trying to pace production to limit exposure to oversaturation. But with rising interest rates, homeowners are facing decreased affordability. This will slow demand for housing to more normal levels.

On top of declining demand, supply challenges from the rising cost of materials and labor will most likely squeeze profit margins for home builders and push them back to pre-pandemic levels. But that has yet to happen.

Based on a peer group analysis of publicly traded home builder margins, gross margins in the first quarter have grown to 27%, up from pre-pandemic levels of 20%. While we do not expect a recurrence of 2007 with a crash in the housing market, there are certainly headwinds that home builders need to continually watch to ensure that they protect their margins and remain profitable.

The takeaway

As rising interest rates increase the cost of owning a home, it appears that we have reached peak market demand and that prices will soon begin to ebb.

The slowing of demand should give builders a chance to deal with some of the supply chain and labor issues they have faced. This slowing of construction will, in turn, result in a decline to lumber prices, bringing them back in line with long-term averages.

While the shifting tides lead to lower margins throughout the supply chain, opportunities are still plentiful. But builders may have to work a little harder to find them.

Let's Talk!

Call us at (325) 677-6251 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Nick Grandy and originally appeared on 2022-06-15.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/how-lumber-tells-the-story-of-home-building-during-the-pandemic/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Condley and Company, LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Condley and Company can assist you, please call (325) 677-6251.