Resources

FOMC decision: Policy, price stability and balance sheet strategy

REAL ECONOMY BLOG | May 04, 2022

Authored by RSM US LLP

Price stability is a precondition of maximum sustainable employment, sustainable growth at the long-term rate of 1.8% and financial stability.

The Federal Open Market Committee’s decision on Wednesday to increase the federal funds rate by a half-percentage point to a range between 0.75% and 1% in tandem with the publication of the central bank’s strategy to reduce its balance sheet imply that the Fed intends to achieve that overarching objective despite the risk of a higher unemployment and a hard landing of the economy.

From our vantage point, the reduction of the balance sheet is indicative of the necessary hawkishness that now permeates monetary policy and will result in a general tightening of financial conditions that will neither please investors nor other policymakers as the economy cools.

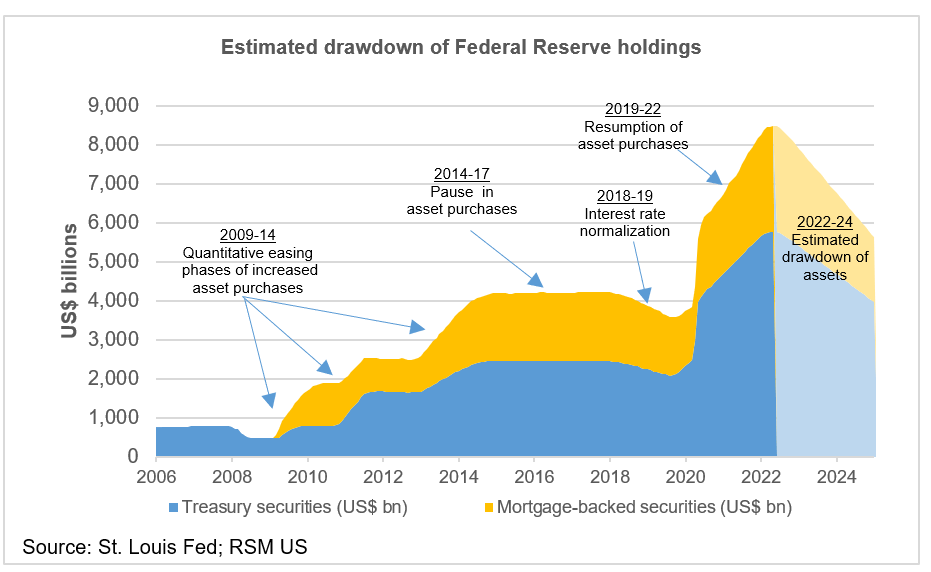

The reduction includes monthly caps of $30 billion in Treasury securities and $17.5 billion in mortgage-backed securities beginning in June that will slowly increase to $60 billion and $35 billion, respectively, in three months

Forward-looking Fed policy and rhetoric have already led investors to price in these changes, resulting in a 10-year Treasury yield hovering around 3% and mortgage rates floating between 5% and 5.5%. These higher rates will cool the red-hot housing market, so we do not anticipate any major resetting of market rates in the aftermath of Wednesday’s decision.

Targeting inflation

The unenumerated target of all this policy is longer-term inflation expectations, which remain remarkably well anchored. Our preferred indicators are the five-year, five-year forward breakeven, which sits just below 2.5% despite the consumer price index hitting 8.5% and the policy-sensitive core personal consumption expenditure deflator reaching 5.1%.

If the Fed is able to retain that rate, it will obtain its policy objective. If it does not, that will require much higher rates, a quicker drawdown of the balance sheet and a much harder landing of the economy than is generally acknowledged.

It is critical for the Fed to follow through on its policy path to restore price stability, even as top-line inflation noticeably eases later this year, and for the Fed to resist the temptation to please fiscal policymakers in the throes of another polarizing political season.

While the utility function of politicians is re-election, central bankers must restore price stability to ensure stable growth and strong employment gains over the coming years, even as the economy is challenged by an unfavorable demographic shift with an aging population and continuing challenges to global supply chains because of geopolitical tensions.

In addition, given the surging costs of shelter and rising wages reflected by the 4.5% increase in the employment cost index on a year-ago basis, the strongest increase in the 20-year history of the metric, the hard-line policy out of the Fed is necessary to keep those expectations anchored and return price stability to the economy.

We expect the Fed to increase its policy rate by an additional 50 basis points at its June meeting and provide an update to its summary of economic projections that will reflect the cooling in the economic activity that lies ahead even as top-line inflation eases noticeably later this year.

Let's Talk!

Call us at (325) 677-6251 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-05-04.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/fomc-decision-policy-price-stability-and-balance-sheet-strategy/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Condley and Company, LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Condley and Company can assist you, please call (325) 677-6251.