Resources

Fed raises its policy rate by 75 basis points and sees more increases

REAL ECONOMY BLOG | September 21, 2022

Authored by RSM US LLP

In the face of growing pressure from policymakers and investors to pause, pivot or even cut its policy rate, the Federal Reserve on Wednesday demonstrated why its independence is the sine qua non of monetary policy.

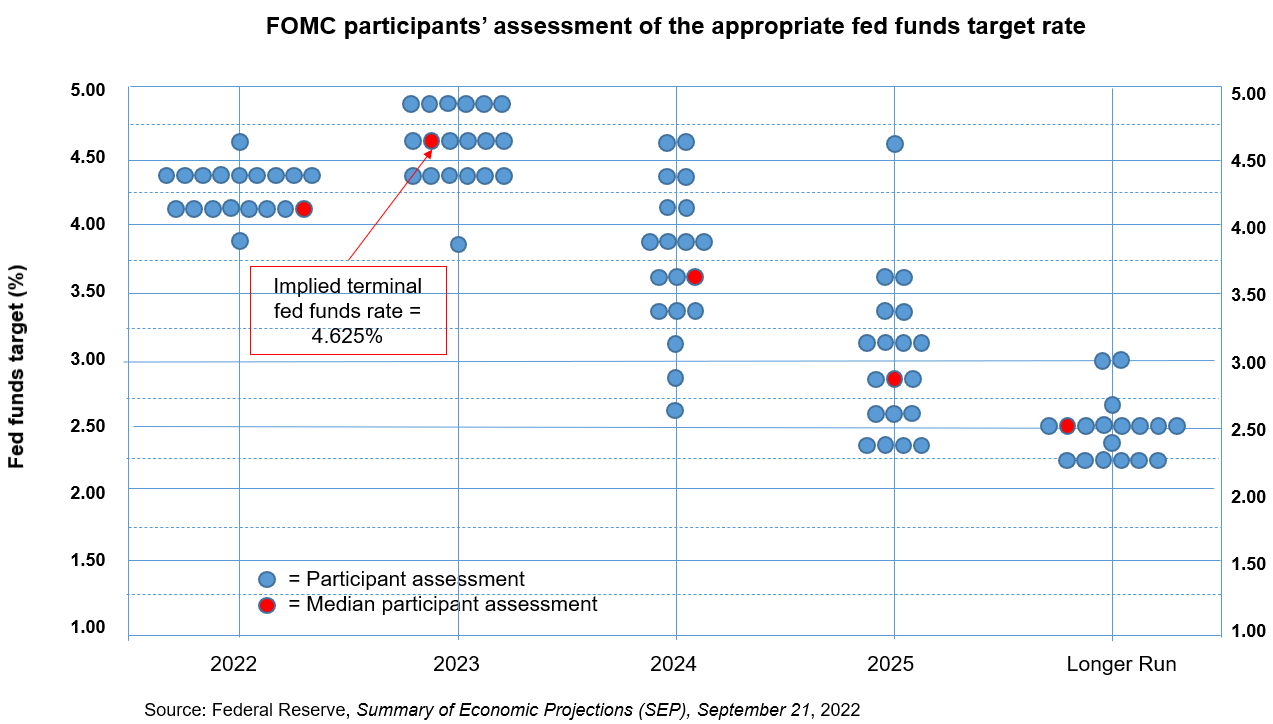

The Fed raised its policy rate by three quarters of a percentage point, to a range of 3% and 3.25%, at the two-day meeting of the Federal Open Market Committee. At the same time, the FOMC’s forecast of rates, or dot plot, projects that the policy rate will reach 4.4% by the end of the year and a terminal rate, or peak, of 4.6% next year. The moves are designed to bring inflation back in linen with the Fed’s target of 2%.

That forecast almost certainly implies another 125 basis points of hikes by the end of the year.

Once the rate reaches 4.6%, the Fed expects rates to ease to 3.9% in 2024 and fall to 2.9% in 2025. But at the end of that time frame, the policy rate will still be above the long-run estimate of the federal funds rate.

Those increases indicate that monetary policy will remain restrictive over the next three years, implying below-trend growth (1.8%) in the economy over that time to restore price stability.

In announcing its rate hike on Wednesday, the Fed also reduced its growth forecasts for 2022 to 2024 and increased its expectation of unemployment, which it forecast will hit a peak of 4.4% in 2023-24.

The Fed also anticipates that the personal consumption expenditures index, a key inflation gauge, will fall to 5.4% by the end of the year, and that core PCE, which strips out more volatile food and energy prices, will be 4.5%.

The Fed expects that these preferred inflation aggregates will not ease back toward its 2% target until 2025.

The Federal Reserve implied in its dot plot that it intends to follow up the September hike with another 75-basis-point increase at the November meeting and a 50-basis-point hike at the December meeting.

Those increases would bring the policy rate to a range between 4.25% and 4.5% by the end of the year.

This policy path will create the conditions for a stronger dollar and add to capital flows into dollar-denominated assets. And those dynamics, in turn, will create inflation issues among critical U.S. trade partners and most likely lead to financial stress in emerging markets.

Given the broadening out of inflation into services and housing, the Federal Reserve has little choice but to act independently to restore price stability despite the risk that it will drive domestic unemployment higher and tip a soft economy into recession.

Our research indicates that the central bank will need to move rates deep into restrictive terrain, causing an increase in the unemployment rate to 4.7% and lead to a loss of 1.7 million jobs. Those job losses would get the inflation rate back down only to 3%.

To get the inflation rate back to the Fed’s 2% goal, job losses could land well above 5.3 million and result in an unemployment rate of 6.7%, at the upper end of the range.

The peak of unemployment at 4.4% inside the Summary of Economic Projections seems somewhat optimistic given the spread of inflation out into the service sector and the fact that the three-month average annualized pace of rents is roughly 9.4%.

It is difficult to accept that, with the delayed impact of past hikes and those that the Fed is now laying out, unemployment will not move higher. Such a move would be in line with our estimate of the sacrifice ratio required to restore price stability.

The takeaway

To restore price stability to the economy, the Federal Reserve will almost certainty continue to push the policy rate higher next year as it continues to reduce its balance sheet, both of which will create tighter financial conditions and a slower pace of growth.

Let's Talk!

Call us at (325) 677-6251 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-09-21.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/fed-raises-its-policy-rate-by-75-basis-points-and-sees-more-increases/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Condley and Company, LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Condley and Company can assist you, please call (325) 677-6251.