Resources

Amid global economic turmoil, stress grips fixed-income markets

REAL ECONOMY BLOG | September 26, 2022

Authored by RSM US LLP

Regime change in the global financial markets and the international economy is in play. Investor and policy expectations around globalization, growth and liquidity are all rapidly changing as central banks lift interest rates to put inflation back in the box.

Fixed-income markets are signaling a shift in perceptions of financial stability and raising a caution flag for investors.

It is highly likely that the American and global economies, which have been characterized by insufficient aggregate demand and low inflation over the past two decades, will now be characterized by insufficient aggregate supply, negative supply shocks, geopolitical tensions and higher inflation.

All of those factors require different monetary and fiscal policies.

This change is showing up in fixed-income markets, which are signaling a shift in perceptions of financial stability and raising a caution flag for investors.

These are the consequences of the oil shock, geopolitical stress and the Federal Reserve’s response to inflation, which in turn are causing global investors to question the durability and direction of globalization, growth and appetite for risk.

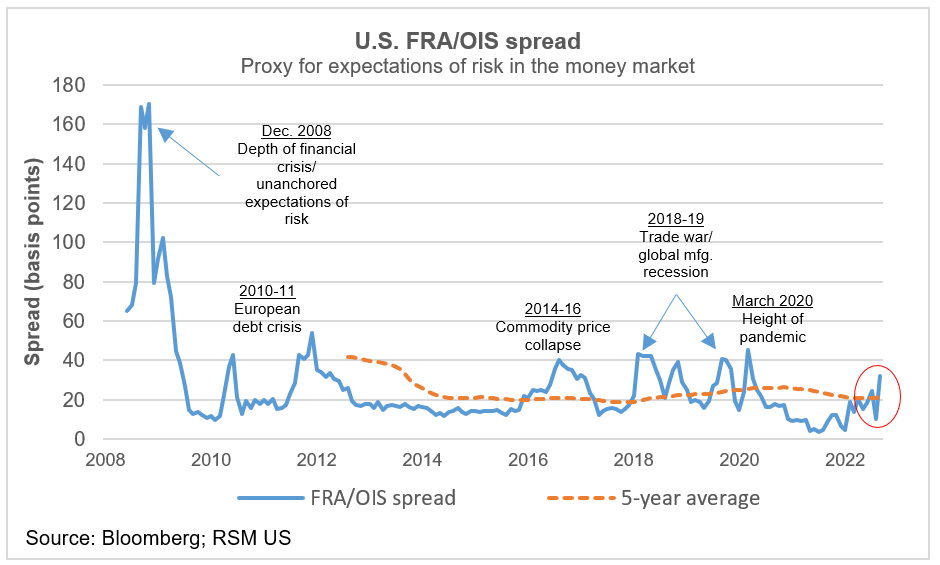

Money market

In the money market, which provides the credit for day-to-day commercial activity, the spread between risk-bearing securities—proxied by forward rate agreements—and the risk-free overnight indexed swaps rate has widened to nearly 30 basis points.

This spread, along with three-month cross-currency basis swaps, are our preferred metrics of global dollar funding stress.

While the spreads have increased, they are nowhere near the depths of the financial crisis or the early days of the pandemic.

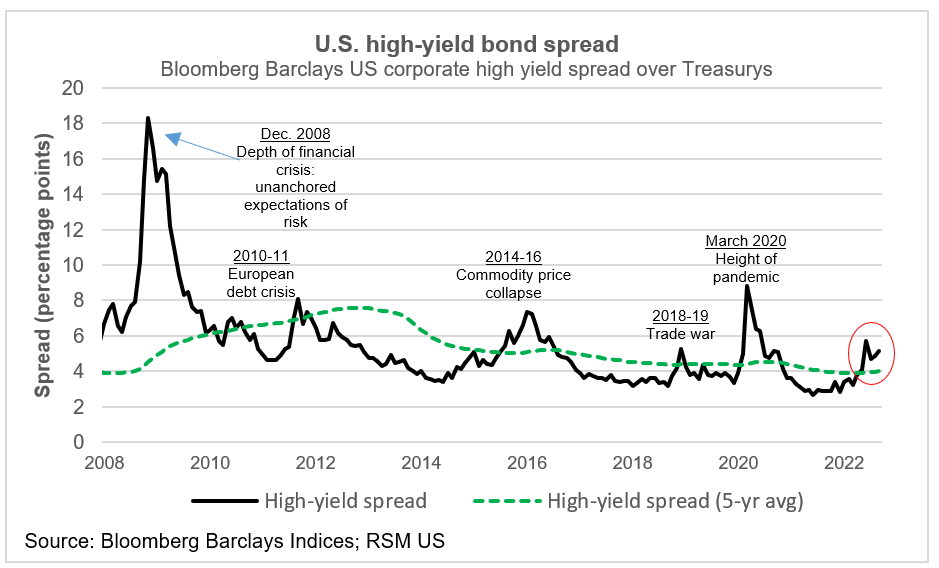

Bond market

In the bond market, the canary in the coal mine is the interest rate spread between riskier high-yield corporate bonds and risk-free Treasury bonds.

As in the money markets, the spread has widened above its five-year moving average. At about five percentage points, it is approaching the levels of earlier crisis episodes. This widening spread requires monitoring by policymakers and investors.

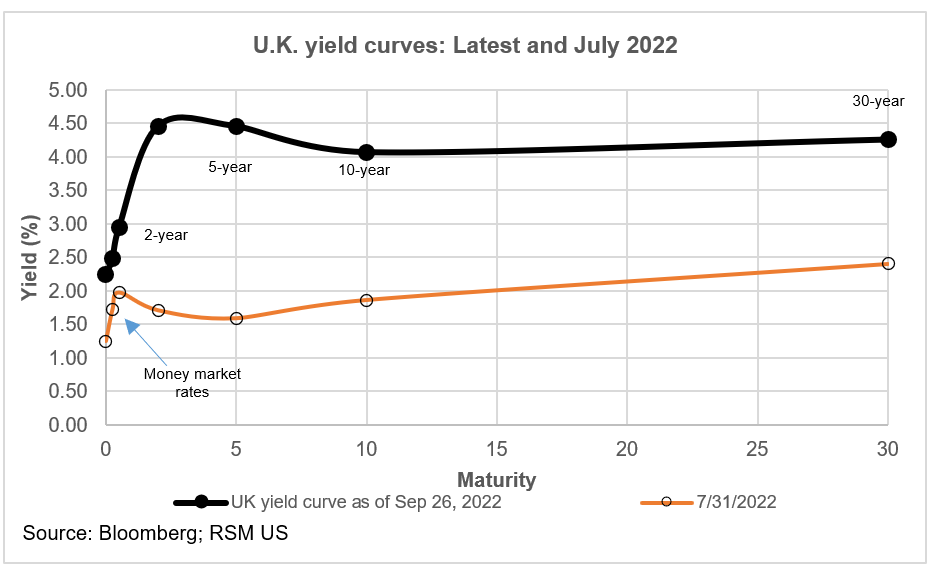

Potential spillover from U.K.

The U.K. foreign exchange and bond markets have reacted to what appears to be a policy mismatch.

In response to the dollar’s strength and the rising cost of energy, the new government is proposing an aggressive fiscal policy of increasing spending through energy subsidies while cutting revenue with tax cuts.

We expect that the Bank of England will provide a statement reaffirming its intent to restore price stability and meet its inflation target over the medium term as well as to engage in an intermeeting rate hike to mitigate the slide of sterling toward parity with the dollar. A 50 basis-point rate hike in the policy rate would be good, a 100-point increase better.

The currency markets see the British government’s expansionary fiscal policies and the Bank of England’s rate increases, which have lagged other central banks, as a recipe for currency weakness. In response, the pound has plunged by nearly 8% in the past two weeks.

And the bond market has pushed the front end of the yield curve higher in anticipation of additional tightening of monetary policy. Two-year gilts are trading at 4.45%, which is 30 basis points higher than 10-year yields at 4.15%.

The takeaway

The U.S. fixed income market is pricing in the shift in monetary policy and the threat of further geopolitical disturbances that will affect the supply chain and the willingness of the financial community to borrow and lend.

We expect the lagged effect of Fed rate hikes to reduce the level of economic activity and output.

The U.K. economy is likely to be more directly affected by the cut-off of Russian energy supplies, with the currency markets assigning more risk to the pound and the bond market reacting to a potential fiscal policy mismatch. Disruptions in the U.K. markets and economy have the potential to spill over into the U.S. markets and economy.

Let's Talk!

Call us at (325) 677-6251 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-09-26.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/amid-global-economic-turmoil-stress-grips-fixed-income-markets/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Condley and Company, LLP is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Condley and Company can assist you, please call (325) 677-6251.